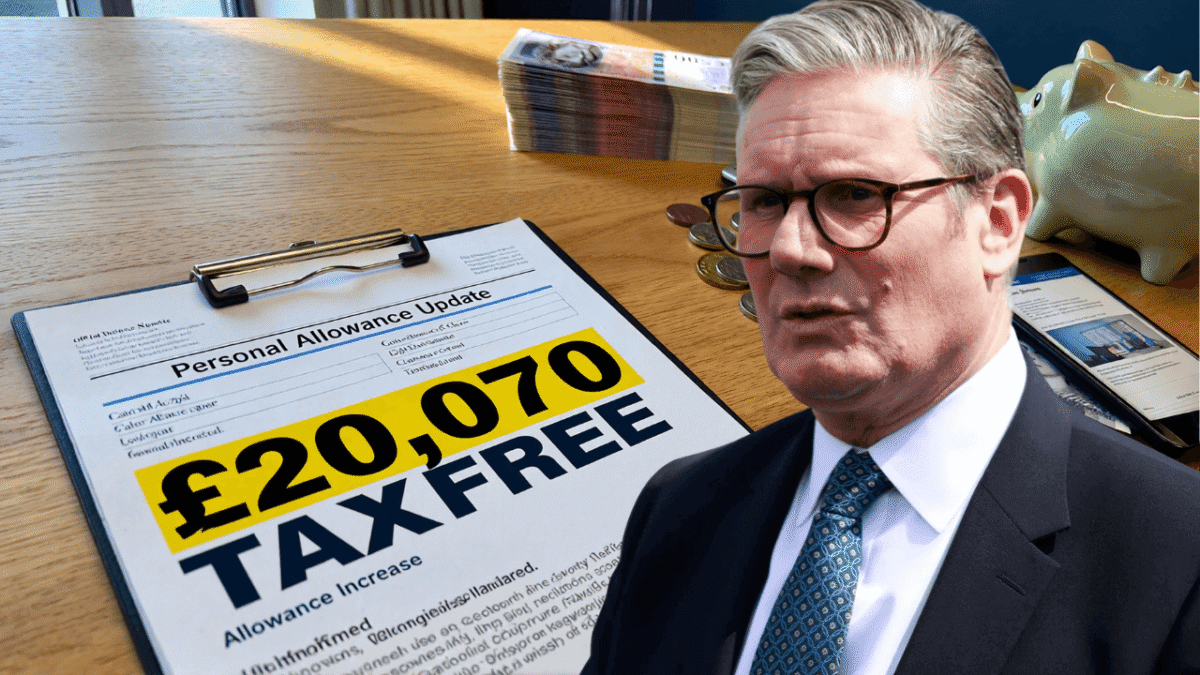

Great news for UK taxpayers: HMRC has officially announced that the personal allowance is increasing to £20,070. This substantial uplift means millions of employees, retirees, and freelancers can enjoy more of their income tax-free. As living expenses continue to climb, this timely adjustment promises to enhance take-home pay and provide essential financial breathing room.

In this detailed breakdown, discover exactly how this change affects your finances, who stands to gain the most, and practical steps to maximize your benefits. Whether you’re on a salary, drawing a pension, or running your own business, understanding these updates is key to smarter money management.

Understanding the UK Personal Tax Allowance

The personal tax allowance forms the foundation of the UK’s income tax framework. It represents the amount of income you can receive each year without owing any income tax, applying to salaries, pensions, and select savings interest.

Managed by HM Revenue & Customs (HMRC), this threshold promotes fairness by shielding basic earnings from taxation. Staying under the limit ensures zero tax liability, acting as a crucial safeguard for everyday finances.

How the Personal Allowance Operates Daily

Any earnings up to the allowance remain entirely tax-free. Income exceeding this point incurs tax at standard rates, beginning at the 20% basic rate.

This tiered approach supports modest and mid-level earners, fostering a balanced tax environment. The new £20,070 figure marks a notable step up from prior thresholds, amplifying its reach.

For employed individuals, the system integrates via PAYE tax codes, which automate withholdings. Freelancers and sole traders reclaim it during Self Assessment filings.

Why the Increase to £20,070 is a Major Win for Taxpayers

This elevation to £20,070 delivers a tangible lift to family budgets across the nation. It shields a larger slice of income from tax, injecting extra cash directly into pockets.

Average earners could pocket several hundred pounds more each year. Amid soaring costs for utilities and food, this relief arrives as a welcome counterbalance.

Historical Background and Policy Drivers

Adjustments to allowances often respond to economic shifts, such as inflation and wage escalation. HM Treasury oversees these evaluations to harmonize taxpayer support with public funding demands.

Previous static periods diminished the allowance’s real value through inflation. This proactive hike restores equilibrium and underscores forward-thinking governance.

- Combats inflation: Safeguards your money’s buying power.

- Aligns with wages: Reflects growing average incomes.

- Ensures balance: Supports services while easing burdens.

Real Impacts on Take-Home Pay for Employees and Self-Employed

Workers will see swift changes in their paychecks as PAYE systems update. Reduced tax deductions translate to higher monthly net income with minimal effort.

Those with salaries between £20,000 and £25,000 might escape basic-rate tax altogether. Self-employed professionals will enjoy lower year-end liabilities through refined calculations.

Practical Savings Examples

Consider a £22,000 annual salary. Before the change, £2,000 would face 20% tax (£400 owed). Now, with £20,070 tax-free, that entire sum stays yours—a clear £400 gain.

Even higher brackets see ripple effects from shifted thresholds. Log into the HMRC portal to verify your tax code and avoid overpayments.

This incentive also spurs greater workforce engagement, letting part-timers extend hours penalty-free and bolstering overall employment.

Key Advantages for Pensioners and Retirees

Retirees receive substantial perks, with the allowance extending to State Pension, occupational plans, and personal savings. For many hovering near the old limit, this erases tax obligations entirely.

Pension income typically offsets against the allowance, streamlining affairs. Modest retirement funds now preserve more value untouched by tax.

Managing Pension Taxes After the Update

The State Pension qualifies as taxable income, yet £20,070 covers it tax-free for most. Pair it with the Marriage Allowance for spouses to unlock up to £1,260 more relief.

- Solo retirees: Secures essentials without deductions.

- Married couples: Share allowances for doubled benefits.

- Extra savings: Add £1,000 PSR for interest-free gains.

Wide-Ranging Economic Effects and Tax Band Insights

Elevating the personal allowance energizes the economy via heightened spending. Extra disposable income fuels shopping, hospitality, and local services.

While some debate revenue impacts, evidence points to growth compensating through activity. HM Treasury projections affirm positive net outcomes.

Other bands persist: 20% basic up to £50,270, 40% higher, and 45% additional. This adjustment curbs fiscal drag, where promotions inadvertently hike tax rates.

Proven Strategies to Optimize Your Finances

Capitalize on this shift by auditing your setup today. Scrutinize payslips, contributions, and holdings for untapped opportunities.

ISAs offer tax-sheltered savings and investments. Ramp up pension deposits for relief rates up to 45%, supercharging growth.

Actionable Steps for Maximum Gains

- Review payslips: Ensure your tax code reflects the new limit.

- Handle Self Assessment: Accurately claim for potential refunds.

- Layer allowances: Include Marriage, Blind Person’s, and others.

- Seek experts: Get tailored advice for intricate cases.

Monitor upcoming Budget reveals and use HMRC tools for projections. Holistic planning—budgeting, saving, investing—amplifies results.

Tax landscapes shift regularly, so sign up for HMRC notifications and Treasury feeds. Sidestep unverified online chatter for reliable intel.

In essence, HMRC‘s endorsement of the £20,070 tax-free personal allowance brings genuine uplift to UK residents. It fortifies pay packets, aids seniors, and invigorates commerce. Seize the moment: assess your position, fine-tune allowances, and gear up for prosperity. Stay vigilant on rollout timelines to fully harness this boon.